Utah Home Improvement Loans: A Guide to Financing Your Dream Home Renovation

Apr 21, 2023

Share

If you're a Utah homeowner in need of home improvement funds, consider using Hitch as your platform. Hitch is home improvement platform that connects homeowners with local contractors and lenders, making it easier to get the funding and resources you need for your dream home renovation. Home improvement loans are one of the financing options available through Hitch, providing Utah homeowners with access to the funds they need to make significant repairs or improvements to their homes, whether it's for updating their kitchen, adding a new bathroom, or even finishing a basement.

Frequently Asked Questions about Home Improvement Loans in Utah

What is a Utah Home Improvement Loan?

A Utah home improvement loan is a type of personal loan that is specifically designed to fund home repairs, renovations, and improvements. Unlike a mortgage or home equity loan, which requires you to use your home as collateral, a home improvement loan is an unsecured loan, meaning you don’t have to put up any collateral to qualify.

Types of Utah Home Improvement Loans

There are two main types of home improvement loans available to Utah homeowners: secured and unsecured loans.

1. Secured loans require collateral, such as your home or another valuable asset, to secure the loan. Because they are secured, these loans typically have lower interest rates than unsecured loans. However, if you fail to make your payments, you could lose your home or other collateral. 2. Unsecured loans, on the other hand, do not require collateral. Instead, they are based on your creditworthiness and ability to repay the loan. Because they are unsecured, these loans typically have higher interest rates than secured loans.

Here are a few examples of the types of home improvement loans available to Utah homeowners:

- Personal Loans - Personal loans are unsecured loans that can be used for a variety of purposes, including home improvements. They typically have higher interest rates than secured loans but may be a good option if you don’t have collateral to secure the loan.

- Home Equity Loans - Home equity loans are secured loans that use your home as collateral. They typically have lower interest rates than personal loans but can be risky if you are unable to make your payments.

- Home Equity Lines of Credit - Home equity lines of credit (HELOCs) are similar to home equity loans but work more like a credit card. You have a line of credit that you can draw from as needed, and you only pay interest on the amount you borrow.

How to Qualify for a Utah Home Improvement Loan

To qualify for a Utah home improvement loan, you’ll typically need to meet the following requirements:

- Have good credit - Most lenders will require you to have a credit score of at least 620 to qualify for a home improvement loan.

- Demonstrate income - You’ll need to show that you have a steady income to make your loan payments.

- Have a plan for your renovation - You’ll need to provide detailed plans and cost estimates for your renovation or repair project.

- Have equity in your home - If you’re applying for a home equity loan or HELOC, you’ll need to have equity in your home.

What are the best ways to locate a home improvement loan in Utah?

To identify the right home improvement loan in Utah, you should consider the different loan types available, such as a personal loan or a home equity loan. Research and compare lenders to get the best interest rate and repayment terms. Also look into any hidden fees that might be associated with each loan type. Make sure to read all the fine print before signing on to any loan agreement. Hitch is an excellent option for home improvement loans in Utah - their competitive interest rates, flexible repayment plans, and free credit counseling make them a great lender for anyone looking for a loan that meets their needs. Additionally, there are no application fees associated with a Hitch home improvement loan so you can start your application process worry-free!

Is obtaining a home improvement loan in Utah a beneficial financing option?

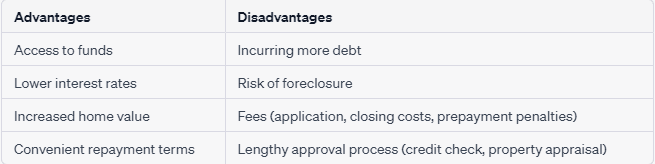

Whether or not a home improvement loan is a worthwhile option for you in Utah depends on your specific situation and financial goals. These loans offer several advantages, such as convenient repayment terms, lower interest rates, and increased home value. However, they also come with potential disadvantages, including fees and the risk of foreclosure. Before deciding on a home improvement loan, it's important to weigh the pros and cons, compare loan offers, and ensure you can comfortably repay the loan according to the agreed-upon terms.

Advantages and Disadvantages of Home Improvement Loans in Utah

If you're a Utah homeowner considering a home improvement project, but lack the necessary funds, a home improvement loan may be a viable financing option. While these loans can provide you with the necessary funds to complete your project, they also come with their own set of advantages and disadvantages. In this article, we'll explore the benefits and drawbacks of home improvement loans in Utah to help you make an informed decision about whether this financing option is right for you.

What steps can you take to determine the most suitable home improvement loan in Utah for your specific financial situation?

To identify the right home improvement loan in Utah, there are several steps you can take.

- Assess your financial situation: Determine your current income, expenses, and credit score to get a clear picture of your financial status.

- Define your project: Determine what type of home improvement project you want to undertake and estimate the cost.

- Shop around: Compare rates and terms from different lenders to find the most favorable loan offers.

- Consider repayment terms: Evaluate the repayment terms of each loan offer, including interest rates, fees, and repayment period.

- Apply for pre-approval: Apply for pre-approval with multiple lenders to obtain personalized loan offers based on your credit score and history.

- Choose the best option: Once you have several offers, compare them and select the loan that best fits your financial situation and project needs.

By taking these steps, you can find a home improvement loan that suits your financial situation and project needs in Utah.

Hitch provides excellent options for home improvement loans in Utah. They offer flexible repayment plans and competitive interest rates that suit your specific financial situation. In addition, Hitch offers free credit counseling and does not charge application fees. You can rely on their excellent customer service and resources to secure a loan that is tailored to your needs and aligns with your budget and lifestyle.

Related Articles:

- Financing Your Colorado Home Improvements: A Guide to Home Improvement Loans with Hitch

- Discover Home Improvement Loans in Oregon with Hitch

- Making Home Improvements Easier in Florida with Hitch Loans

- Exploring Home Improvement Loans for Home Repair and Renovations in California

- Home Improvement Loans in Nevada: What You Need to Know

- Exploring Home Improvement Loan Options in Arizona

- Renovations, remodeling, and additions loan calculator

- FAQ

Hitch, Inc. NMLS #2383367 #2383367

2158 NW Toussaint Drive. Bend, Oregon 97703

1. Qualified applicants may borrow up to 95% of their home’s value. This does not apply to investment properties.

2. HELOCs have a 10-year draw period. During the draw period, the borrower is required to make monthly minimum payments, which will equal the greater of (a) $100; or (b) the total of all accrued finance charges and other charges for the monthly billing cycle. During the draw period, the monthly minimum payments may not reduce the outstanding principal balance. During the repayment period, the borrower is required to make monthly minimum payments, which will equal the greater of (a) $100; or (b) 1/240th of the outstanding balance at the end of the draw period, plus all accrued finance charges and other fees, charges, and costs.The lender will calculate this amount by taking the outstanding Account Balance on the last day of the draw period and dividing it by 240 months and then adding any finance charge that accrues but remains unpaid during the monthly billing cycle plus any other fees, charges and costs to the fixed principal payment that is due. During the repayment period, the monthly minimum payments may not, to the extent permitted by law, fully repay the principal balance outstanding on the HELOC. At the end of the repayment period, the borrower must pay any remaining outstanding balance in one full payment.

3. The time it takes to get cash is measured from the time the Lending Partner receives all documents requested from the applicant and assumes the applicant’s stated income, property and title information provided in the loan application matches the requested documents and any supporting information. Most borrowers get their cash on average in 21 days. The time period calculation to get cash is based on the first 4 months of 2024 loan funding's, assumes the funds are wired, excludes weekends, and excludes the government-mandated disclosure waiting period. The amount of time it takes to get cash will vary depending on the applicant’s respective financial circumstances and the Lending Partner’s current volume of applications. Closing costs can vary from 3.0 - 5.0%. An appraisal may be required to be completed on the property in some instances.

4. Not all borrowers will meet the requirements necessary to qualify. Rates and terms are subject to change based on market conditions and borrower eligibility. This offer is subject to verification of borrower qualifications, property evaluations, income verification and credit approval. This is not a commitment to lend.

5. The content provided is presented for information purposes only. This is not a commitment to lend or extend credit. Information and/or dates are subject to change without notice. All loans are subject to credit approval. Other restrictions may apply.