Financing Your Colorado Home Improvements: A Guide to Home Improvement Loans

Apr 18, 2023

Share

If you're a homeowner in Colorado, you may be considering home improvements to make the most of the state's sunny summers and snowy winters. Popular upgrades include sunrooms, covered patios, and other repairs or renovations to keep your home comfortable in all seasons. It's especially important to ensure your HVAC system is working properly before the heat of summer or cold of winter sets in. To finance these costly projects, many homeowners turn to home improvement loans. Hitch can help you navigate the options available and find the best loan to fit your needs. Keep reading to learn more about home improvement loans in Colorado.

Assisting Colorado Homeowners with Home Improvement Loans

Homeowners in Colorado experience varying weather patterns from snowy winters to sunny summers, leading to different home improvement needs. From roof repairs to upgrading HVAC systems, homeowners in Colorado require financial assistance to make their homes comfortable and secure. Hitch provides an easy and straightforward way to explore various loan options for home improvements in Colorado. Keep reading to learn more about home improvement loans in Colorado.

What is the process for obtaining home improvement loans in Colorado?

Colorado homeowners have various options to finance home improvement projects. The loan type that works best for each individual can differ due to the varying requirements of each loan. If you own your home in Colorado, you may want to consider a home equity loan, home equity line of credit, or a secured or unsecured personal home improvement loan. These loan types are specifically designed to provide funding for renovations, upgrades, or repairs on your home. Let's take a closer look at how each loan works in Colorado:

-

Home equity loan: With a minimum of 20% equity in your home, you can borrow up to 85% of that equity in the form of a home equity loan. This loan is available to you when the mortgage balance on your home is equal to or less than 80% of the home's appraised value.

-

Home equity line of credit: If you have at least 20% equity in your home, you may be eligible for a revolving line of credit known as a home equity line of credit. A lender can provide you with a credit line with a credit limit depending on the amount of equity you have in your home. You can borrow as much or as little of that credit line as you need to finance your home remodeling project. Interest is only charged on the amount borrowed, and you can borrow again at a future date, much like a credit card.

-

Unsecured personal home improvement loan: If you have good creditworthiness, you can get an unsecured personal home improvement loan with loan amounts up to $100,000. There is no collateral required for these loans, and you can compare offers without affecting your credit score at Hitch. Loans are typically funded as a lump sum minus fees and repaid in fixed monthly installments with interest.

-

Secured personal home improvement loans: These loans work similarly to unsecured loans, but they require collateral. This means they may take longer to fund and pose a higher risk for borrowers.

-

Section 504 Home Repair Program: This program offers a loan of up to $40,000 for low-income homeowners to repair, modernize, or improve their homes. Elderly homeowners can also receive a grant of up to $10,000 to remove health and safety hazards from their homes.

For those looking to buy an older home and renovate it in Colorado, there are several home renovation loan options available. Here's a breakdown of commonly used loans:

-

Fannie Mae Homestyle Renovation Mortgage: With down payments as low as 3%, borrowers with a minimum credit score of 720 or higher can obtain up to 75% of the estimated post-renovation appraisal value. Borrowers with a credit score as low as 680 may need to put in a down payment of up to 25%. Loans come with terms of either 15 or 30 years, and all home improvements must be completed within 12 months of the mortgage closing.

-

Freddie Mac CHOICE Renovation Mortgage: This loan program is for individuals looking to purchase and rehabilitate, renovate, repair, or restore an existing home. Borrowers with credit scores of 720 or higher may qualify for the loan with only a required down payment of 5%. Those with credit scores as low as 620 may need a down payment of up to 25%. Loan terms can be 15, 20, or 30 years.

-

FHA 203(k) Mortgage: This loan program is a good option for borrowers with lower credit scores who want to buy an older home and renovate it. FHA 203(k) loans require a 3.5% down payment for borrowers with a credit score of 580 or higher, and a down payment of 10% for those with a credit score between 500 and 579. These loans can be for up to 110% of the estimated home value after renovations are completed. Loan terms can be for 15, 20, 25, or 30 years.

-

VA Renovation Loan: VA renovation loans are reserved for veterans, surviving spouses, or active duty service members with a minimum credit score of 620 who need funds to renovate an older home. All work must be completed by VA-approved contractors since the funds are paid directly to the contractors by the federal government. Little to no down payment is required, and closing costs are limited. Compare offers with no credit impact at Hitch.

What are the steps to apply for a home improvement loan in Colorado?

If you are considering a home improvement loan in Colorado, the first step is to determine which type of loan is best suited for your needs. Once you have decided, you can start to research lenders who specialize in the loan type you are interested in. Hitch is a great resource for comparing loan offers with no impact on your credit score. After you have found a few lenders that interest you, you can fill out a prequalification application to determine your eligibility and get personalized loan offers. The loan offers will provide you with important details such as interest rates, monthly payments, and any fees associated with the loan. By comparing offers side-by-side, you can choose the best lender and loan for your specific needs.

What is the process of discovering the suitable home improvement loan in Alabama?

To find the ideal home improvement loan in Colorado, it's crucial to look beyond the advertised rates and consider the rates you're eligible for based on your credit score and history. A helpful approach is to compare various loan offers, although bear in mind that doing so may affect your credit score. Hitch is an excellent resource for exploring offers as they can connect you to a network of premier national lenders who provide customized home improvement loan offers without any impact on your credit score.

Discover the Best Home Improvement Loans in Colorado with Hitch

Discovering the appropriate home improvement loan in Colorado can be an arduous and time-consuming task. Fortunately, Hitch has simplified the process of finding the right loan. By exploring offers from their trusted network of lenders, you can easily find the best loan for your needs without any impact on your credit score. If you're a homeowner in Colorado looking for the right home improvement loan, consider these valuable tips.

Get to know further about Home Improvement Loan in Colorado:

What are the most beneficial applications of a home improvement loan in Colorado?

While a home improvement loan in Colorado can be used for any home improvement project, it is wise to allocate the funds towards projects that offer a high return on investment, such as upgrades to your home's infrastructure, plumbing, electrical or HVAC systems, or renovations that enhance the functionality and appearance of your property.

What is the maximum loan amount for a home improvement loan in Colorado?

Personal home improvement loans typically have a maximum loan amount of $100,000 in Colorado, although this may differ by lender. The maximum amount that you qualify for will depend on your credit score, eligibility criteria and other loan terms. If you opt for secured home improvement loans, you may be able to borrow higher amounts based on the collateral you provide. For exploring offers from top lenders in Colorado, consider Hitch as a reliable resource.

What are the prerequisites to obtain a home improvement loan in Colorado?

The eligibility criteria for a home improvement loan can differ based on the type of loan and the lender you choose. For instance, loans that are secured based on your home's value and equity will require you to own a home and undergo a home appraisal to verify the equity. Some fundamental requirements for both secured and unsecured home improvement loans in Colorado include a credit score, a reasonable debt-to-income ratio, stable employment, an active bank account, financial stability, and a decent credit history. If you're a Colorado resident seeking a home improvement loan that meets your eligibility criteria, Hitch can help you explore offers from top lenders.

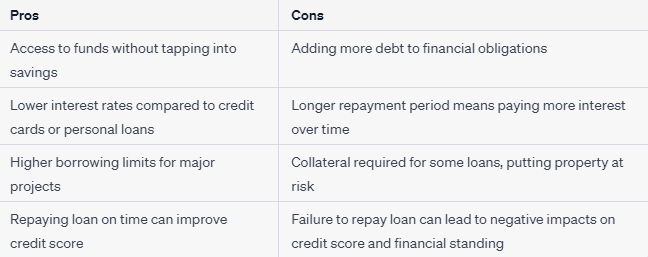

Pros and Cons of Home Improvement Loans in Colorado

Home improvement loans in Colorado come with their own set of benefits and drawbacks that homeowners should consider before deciding to take out a loan. Here are some examples of the advantages and disadvantages:

If you're considering a home improvement project in Colorado, Hitch is a great platform to explore your financing options. With a network of trusted lenders, you can compare offers without impacting your credit score and find the loan that fits your unique needs and budget. Whether you're looking to renovate your kitchen, add a new bathroom, or make energy-efficient upgrades to your home, Hitch can help you find the right home improvement loan. Start exploring your options today and take the first step towards achieving your home improvement goals.

Related Articles:

- Discover Home Improvement Loans in Oregon with Hitch

- Making Home Improvements Easier in Florida with Hitch Loans

- Exploring Home Improvement Loans for Home Repair and Renovations in California

- Home Improvement Loans in Nevada: What You Need to Know

- Renovations, remodeling, and additions loan calculator

- FAQ

Hitch, Inc. NMLS #2383367 #2383367

2158 NW Toussaint Drive. Bend, Oregon 97703

1. Qualified applicants may borrow up to 95% of their home’s value. This does not apply to investment properties.

2. HELOCs have a 10-year draw period. During the draw period, the borrower is required to make monthly minimum payments, which will equal the greater of (a) $100; or (b) the total of all accrued finance charges and other charges for the monthly billing cycle. During the draw period, the monthly minimum payments may not reduce the outstanding principal balance. During the repayment period, the borrower is required to make monthly minimum payments, which will equal the greater of (a) $100; or (b) 1/240th of the outstanding balance at the end of the draw period, plus all accrued finance charges and other fees, charges, and costs.The lender will calculate this amount by taking the outstanding Account Balance on the last day of the draw period and dividing it by 240 months and then adding any finance charge that accrues but remains unpaid during the monthly billing cycle plus any other fees, charges and costs to the fixed principal payment that is due. During the repayment period, the monthly minimum payments may not, to the extent permitted by law, fully repay the principal balance outstanding on the HELOC. At the end of the repayment period, the borrower must pay any remaining outstanding balance in one full payment.

3. The time it takes to get cash is measured from the time the Lending Partner receives all documents requested from the applicant and assumes the applicant’s stated income, property and title information provided in the loan application matches the requested documents and any supporting information. Most borrowers get their cash on average in 21 days. The time period calculation to get cash is based on the first 4 months of 2024 loan funding's, assumes the funds are wired, excludes weekends, and excludes the government-mandated disclosure waiting period. The amount of time it takes to get cash will vary depending on the applicant’s respective financial circumstances and the Lending Partner’s current volume of applications. Closing costs can vary from 3.0 - 5.0%. An appraisal may be required to be completed on the property in some instances.

4. Not all borrowers will meet the requirements necessary to qualify. Rates and terms are subject to change based on market conditions and borrower eligibility. This offer is subject to verification of borrower qualifications, property evaluations, income verification and credit approval. This is not a commitment to lend.

5. The content provided is presented for information purposes only. This is not a commitment to lend or extend credit. Information and/or dates are subject to change without notice. All loans are subject to credit approval. Other restrictions may apply.