Discover Home Improvement Loans in Oregon

Apr 18, 2023

Share

Assisting Oregon Homeowners in Obtaining Home Improvement Loans

Oregon homeowners experience mild summers and wet winters in the Pacific Northwest, making home improvements such as insulation upgrades or roof repairs a priority. To cover the expenses of costly repairs and home improvement projects in Oregon, homeowners often seek home improvement loans. Read on for further details on home improvement loans in Oregon.

Home Improvement Loans in Oregon: Frequently Asked Questions

Are you an Oregon homeowner looking to make renovations or repairs on your home? Home improvement loans may be a great option for you. However, there are several factors to consider before selecting the best type of loan for your needs. Let's take a look at some frequently asked questions about home improvement loans in Oregon.

How do home improvement loans work in Oregon?

Similar to Alabama, Oregon offers several types of home improvement loans for homeowners. These include home equity loans, home equity lines of credit, unsecured personal home improvement loans, secured personal home improvement loans, and Section 504 Home Repair Program loans.

A home equity loan allows you to borrow up to 85% of the equity in your home if you have a minimum of 20% equity. A home equity line of credit allows you to borrow as much or as little as you need, up to your credit limit, and only pay interest on the amount borrowed. Unsecured personal home improvement loans, such as those available through Hitch, offer loan amounts up to $100,000, depending on your creditworthiness, with no collateral required. Secured personal home improvement loans work similarly to unsecured loans but are secured by collateral, which may take longer to fund and involve more risk for the borrower. The Section 504 Home Repair Program offers loans of up to $40,000 or grants of up to $10,000 for eligible homeowners.

For those looking to purchase an older home and renovate it, Oregon offers home renovation loans such as the Fannie Mae Homestyle Renovation Mortgage, the Freddie Mac CHOICERenovation Mortgage, the FHA 203(k) Mortgage, and the VA Renovation Loan.

If you are interested in obtaining an unsecured personal home improvement loan, compare offers with no credit impact at Hitch.

What is the Fannie Mae Homestyle Renovation Mortgage?

The Fannie Mae Homestyle Renovation Mortgage is a loan that allows you to borrow up to 75% of the estimated post-renovation appraisal value. Borrowers with a minimum credit score of 720 may be eligible for down payments as low as 3%. Borrowers with a credit score as low as 680 may be required to put in a down payment of up to 25%. Loan terms are either 15 or 30 years, and all home improvements must be completed within 12 months of the mortgage closing.

What is the Freddie Mac CHOICERenovation Mortgage?

The Freddie Mac CHOICERenovation Mortgage is a loan program designed for individuals looking to purchase and renovate an existing home. Borrowers with credit scores of 720 or higher may qualify for the loan with only a required down payment of 5%. Borrowers with a credit score as low as 620 may need a down payment of up to 25%. Loan terms can be 15, 20, or 30 years.

What is the FHA 203(k) Mortgage?

The FHA 203(k) Mortgage is a loan program for borrowers with lower credit scores who are looking to purchase an older home and renovate it. Borrowers with a credit score of 580 or higher may qualify for the loan with a 3.5% down payment, while borrowers with a credit score between 500 and 579 may need a down payment of 10%. These loans can be for up to 110% of the estimated home value after the renovations are completed. Loan terms can be for 15, 20, 25, or 30 years.

What is the VA Renovation Loan?

The VA Renovation Loan is a loan program reserved for veterans, surviving spouses, or active duty service members with a minimum credit score of 620. The loan is designed for those in need of funds to renovate an older

What are the steps to apply for a home improvement loan in Oregon?

To apply for a home improvement loan in Oregon, the first step is to figure out the type of loan that suits your needs. Once you have determined the loan type, you can start searching for lenders who specialize in it. Whether you require a personal home improvement loan or a home equity loan, the next step is to prequalify. Prequalifying involves completing an application that will allow you to receive personalized loan offers from lenders. These offers will detail how much you can expect to pay in interest, monthly payments, and any other potential fees. You can compare the loan offers side-by-side and select the one that suits your requirements best. Hitch can help you explore personalized loan offers from top national lenders, without impacting your credit score.

Can you suggest ways to choose the right home improvement loan in Oregon?

Advertised rates are one thing - but real rates you qualify for are another. The best way to find the best home improvement loan in Oregon based on your actual credit score and history is to compare offers. Checking offers can sometimes impact your credit score so be aware of that when applying for loans. One of the best ways to choose the right home improvement loan is to start by exploring offers at Hitch. Our network of top national lenders can extend personalized home improvement loan offers with no credit impact!

What are the best uses for a home improvement loan in Oregon?

A home improvement loan in Oregon can be utilized for a wide range of home improvement projects. However, it is recommended to use the funds for projects that offer a high return on investment. This may include projects such as kitchen or bathroom renovations, roof repairs or replacements, HVAC upgrades, and energy-efficient home improvements. Hitch can help you find personalized loan offers from top national lenders to help finance your home improvement project.

Can you suggest some low-cost home improvement ideas?

Personal home improvement loans typically have a maximum loan amount of $100,000, but this can vary depending on the lender. The maximum loan amount you qualify for will depend on your credit score and other requirements. If you opt for a secured home improvement loan, you may be able to access higher loan amounts. Hitch, our lending partner, can help you explore your options and find a loan that fits your needs.

Could you list the requirements to qualify for a home improvement loan in Oregon?

There are different requirements for different home improvement loans depending on the loan type and lender in Oregon. For instance, home improvement loans that are based on the value of your home and the amount of equity you have in it require you to already own your own home to qualify. Additionally, a home appraisal may be needed to validate the equity. The following are some basic requirements for secured and unsecured home improvement loans in Oregon:

- Credit score

- Debt-to-income ratio

- Employment

- Bank account

- Collateral (if secured)

- Financial stability

- Credit history

Discover which lenders you qualify for by checking out offers at Hitch.

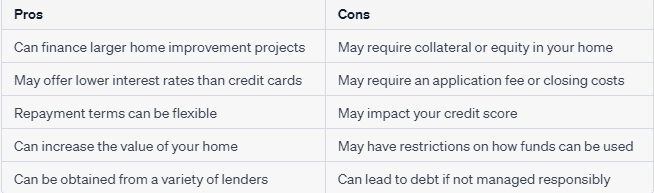

Pros & Cons of Home Improvement Loans in Oregon

Like any financial product, home improvement loans in Oregon come with their own set of advantages and disadvantages. Here are some of the pros and cons to consider:

If you are planning to finance your home improvement project in Oregon, Hitch can be a great platform to explore your options. With their network of top national lenders, you can easily compare personalized loan offers without impacting your credit score. Plus, their user-friendly interface makes it easy to apply and get approved for the loan that best fits your needs. Consider checking out Hitch today and take the first step towards making your home improvement dreams a reality.

Related Articles:

Hitch, Inc. NMLS #2383367 #2383367

2158 NW Toussaint Drive. Bend, Oregon 97703

1. Qualified applicants may borrow up to 95% of their home’s value. This does not apply to investment properties.

2. HELOCs have a 10-year draw period. During the draw period, the borrower is required to make monthly minimum payments, which will equal the greater of (a) $100; or (b) the total of all accrued finance charges and other charges for the monthly billing cycle. During the draw period, the monthly minimum payments may not reduce the outstanding principal balance. During the repayment period, the borrower is required to make monthly minimum payments, which will equal the greater of (a) $100; or (b) 1/240th of the outstanding balance at the end of the draw period, plus all accrued finance charges and other fees, charges, and costs.The lender will calculate this amount by taking the outstanding Account Balance on the last day of the draw period and dividing it by 240 months and then adding any finance charge that accrues but remains unpaid during the monthly billing cycle plus any other fees, charges and costs to the fixed principal payment that is due. During the repayment period, the monthly minimum payments may not, to the extent permitted by law, fully repay the principal balance outstanding on the HELOC. At the end of the repayment period, the borrower must pay any remaining outstanding balance in one full payment.

3. The time it takes to get cash is measured from the time the Lending Partner receives all documents requested from the applicant and assumes the applicant’s stated income, property and title information provided in the loan application matches the requested documents and any supporting information. Most borrowers get their cash on average in 21 days. The time period calculation to get cash is based on the first 4 months of 2024 loan funding's, assumes the funds are wired, excludes weekends, and excludes the government-mandated disclosure waiting period. The amount of time it takes to get cash will vary depending on the applicant’s respective financial circumstances and the Lending Partner’s current volume of applications. Closing costs can vary from 3.0 - 5.0%. An appraisal may be required to be completed on the property in some instances.

4. Not all borrowers will meet the requirements necessary to qualify. Rates and terms are subject to change based on market conditions and borrower eligibility. This offer is subject to verification of borrower qualifications, property evaluations, income verification and credit approval. This is not a commitment to lend.

5. The content provided is presented for information purposes only. This is not a commitment to lend or extend credit. Information and/or dates are subject to change without notice. All loans are subject to credit approval. Other restrictions may apply.